How Far behind on Car Payments: Avoid Repossession!

Facing the possibility of car repossession can be incredibly stressful. If you’re worried about falling behind on your car payments, you’re not alone.

Many people find themselves in this situation, wondering how far they can go before facing the dreaded tow truck. Understanding the timeline and actions you can take might be the difference between keeping your car or losing it. In this guide, we’ll explore the crucial details you need to know to stay ahead of repossession.

You’ll discover practical steps to manage your payments and gain peace of mind. So, if you’re eager to protect your car and your credit score, keep reading to find out how you can take control of your financial future.

Signs Of Imminent Repossession

Trouble with car payments often signals repossession risks. Falling behind by two or three months raises red flags. Expect the lender’s action as financial responsibilities are neglected.

Facing the possibility of car repossession can be a stressful experience. Knowing the signs of imminent repossession can help you take proactive steps to avoid losing your vehicle. It’s crucial to recognize these warning signals to protect your financial stability and peace of mind.1. Receiving Persistent Payment Reminder Calls

One of the earliest signs is a barrage of phone calls from your lender. They won’t just disappear if you ignore them. These calls are reminders that you’re behind and need to act. Answering these calls can sometimes provide opportunities to negotiate payment terms.2. Notice Of Default In The Mail

Lenders typically send a Notice of Default when you’re significantly behind on payments. This document officially informs you of your overdue status and potential legal actions. Ignoring this notice can escalate the situation, leading to repossession.3. Locked Out Of Online Account

If you’ve been denied access to your online account, it might be a sign that the lender is preparing for repossession. They might restrict access to prevent you from making changes or accessing information. This is a critical moment to contact your lender and discuss your options.4. Repo Agent Scouting Your Neighborhood

Some individuals have shared their surprise at seeing unfamiliar vehicles slowly cruising their neighborhood. This could be a repo agent assessing the situation. If you notice this, it’s a clear signal to urgently address your payment issues.5. Decline In Credit Score

A sudden drop in your credit score can indicate missed payments. While you might not check your score regularly, staying informed can help you anticipate potential actions from your lender. Monitoring your credit can also help you address other financial issues early.6. Receiving Legal Notices

In some jurisdictions, lenders must send legal notices before repossessing your car. These documents are serious and require immediate attention. Consulting a legal expert can provide clarity and help you understand your rights. — Have you noticed any of these signs recently? Recognizing them early can make all the difference. What steps will you take today to prevent repossession and safeguard your financial future?Assessing Your Financial Situation

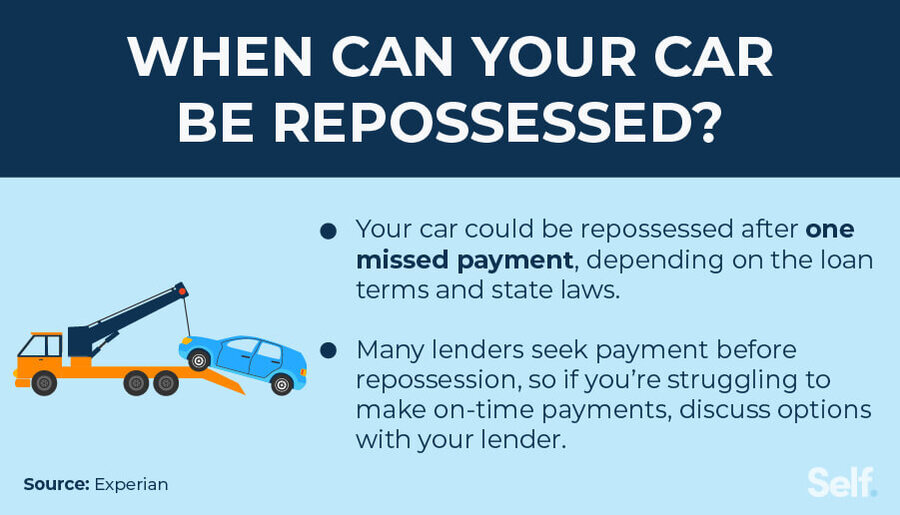

Car payments falling behind can lead to car repossession. Usually, missing several payments triggers this process. Each lender has different rules, so check your loan agreement for specifics.

Assessing your financial situation is a critical step when you find yourself falling behind on car payments. It’s not just about numbers on a page; it’s about understanding your current financial landscape and making informed decisions. By evaluating your finances, you can identify areas where adjustments can be made to potentially avoid repossession.Understanding Your Income And Expenses

The first step is to clearly define your monthly income and expenses. Do you know exactly how much money comes in and goes out each month? Create a simple list to track your income sources and a separate list for expenses. This clarity can be eye-opening and will help you pinpoint where you can cut back. Sometimes, the smallest changes can free up significant funds to cover your car payments.Prioritizing Essential Payments

Consider which expenses are essential and which ones can be reduced or temporarily eliminated. Are you spending more on dining out than on your car payment? It’s important to prioritize your car payments over non-essential spending. This prioritization ensures that you’re covering necessary expenses while looking for areas to save money.Exploring Additional Income Sources

Have you thought about ways to increase your income temporarily? Many people find success with part-time jobs or freelance gigs. It can be a way to bridge the gap between your current financial situation and your car payment obligations. Explore skills you have that could be monetized. Even a few extra hours a week can make a difference.Evaluating Savings And Assets

Do you have savings or assets that can be utilized? This might be the right time to tap into emergency funds if they exist. If you have items of value that you’re willing to sell, this could provide immediate relief. Think about assets that aren’t essential to your daily living and see if they could be converted into cash to cover the payments.Seeking Professional Financial Advice

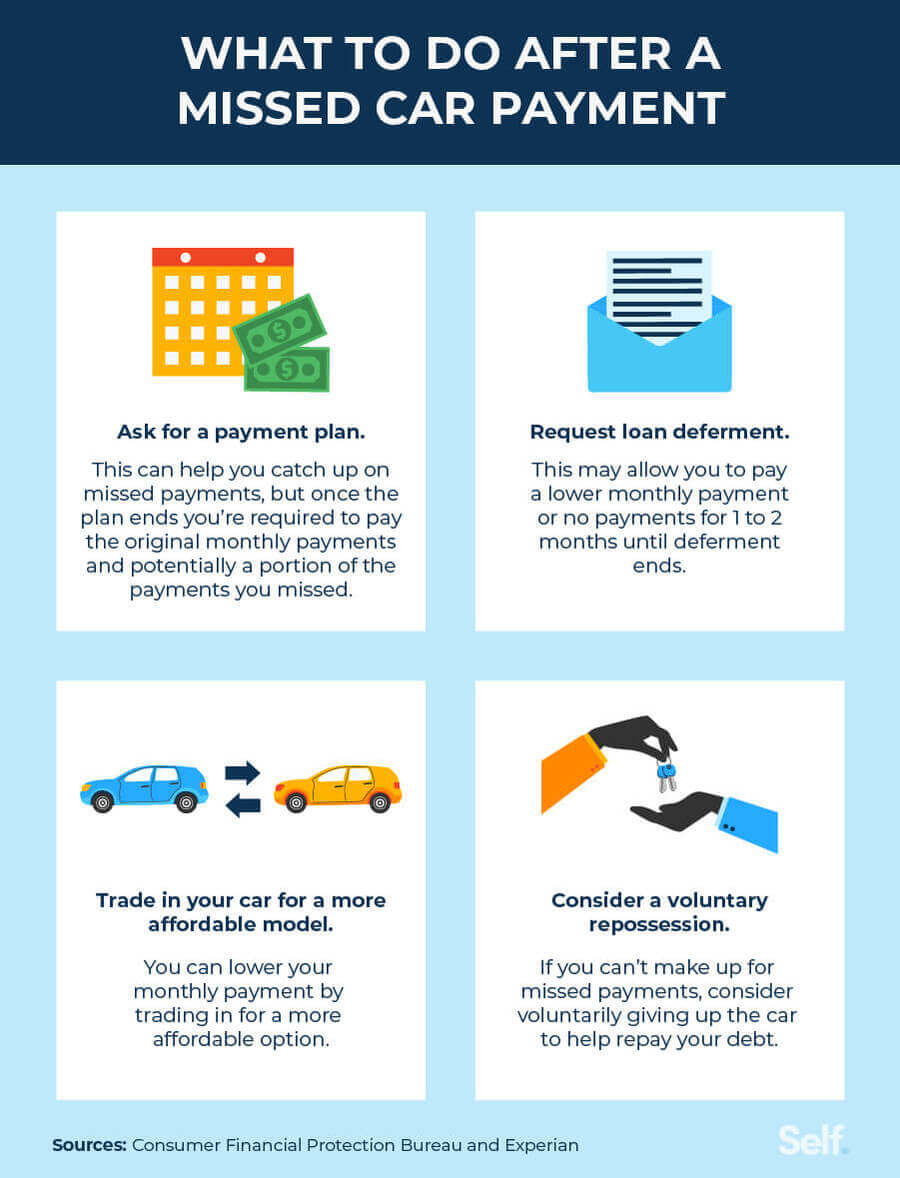

Sometimes, the situation might require outside help. Have you considered consulting a financial advisor? Professionals can offer insights you might not have thought about. They can help you restructure your budget or suggest programs you qualify for to ease your financial burden. Seeking advice is not a sign of weakness; it’s a proactive step towards financial stability. — By thoroughly assessing your financial situation, you can gain control and make decisions that may prevent repossession. Remember, the goal is to understand your finances clearly and to act before reaching a critical point. What steps will you take today to secure your financial future?Communicating With Your Lender

Communicating with your lender is crucial when you’re behind on car payments. Often, borrowers hesitate to reach out due to fear or embarrassment. However, taking the initiative to talk to your lender can be the key to avoiding repossession. You might be surprised at how willing lenders are to work with you if you show them you’re committed to resolving the issue.

Importance Of Early Contact

Contact your lender as soon as you realize you’ll miss a payment. Early communication can prevent misunderstandings and build trust. When you reach out early, lenders are more likely to see you as proactive rather than negligent.

Imagine being a lender. Would you prefer a borrower who hides from you or one who acknowledges their situation and seeks solutions? By contacting them early, you demonstrate responsibility and open the door to potential solutions.

Negotiating Payment Plans

Once you’ve made contact, discuss possible payment plans. Lenders often have options for restructuring your debt. They might offer to adjust your payment schedule or reduce the monthly amount temporarily.

Consider sharing your story with the lender. Explain why you’re struggling and how you plan to get back on track. This personal touch can be persuasive and show your commitment to resolving the situation.

Have you ever thought about what could happen if you ignore the problem? By negotiating a payment plan, you can avoid the stress and financial burden of repossession. Lenders want to avoid repossession as much as you do, so they are likely to work with you.

Remember, your lender is not just a faceless corporation. They are people who understand financial difficulties. Show them you’re willing to cooperate, and you might find more flexibility than you expected.

Credit: www.self.inc

Exploring Refinancing Options

Facing late car payments raises repossession risks. Lenders often start actions after two missed payments. Exploring refinancing options can provide relief.

Falling behind on car payments can be stressful, and the looming threat of repossession might feel overwhelming. However, you have options to consider that could ease your financial burden, such as refinancing. Refinancing your car loan can be a strategic move to keep your vehicle and regain control over your finances. Let’s dive into the benefits and how to find the right lender.Benefits Of Refinancing

Refinancing can potentially lower your interest rate, which means you could pay less over time. Imagine saving hundreds or even thousands of dollars simply by securing a better rate. This extra cash can alleviate some of the financial pressure you’re facing. You might also reduce your monthly payments, making it easier to manage your budget. If your current payment feels like a burden, a lower payment could bring much-needed relief. Additionally, refinancing can extend the term of your loan. While it may mean paying longer, spreading out payments can make them more manageable and avoid repossession.Finding The Right Lender

Selecting the right lender is crucial. Not all lenders offer the same terms, so it’s important to shop around. Consider banks, credit unions, and online lenders—each may provide different advantages. Look for lenders with a solid reputation. Read reviews, ask for recommendations, and check their customer service track record. Trustworthy lenders are transparent about fees and terms. Compare interest rates and fees. A lower rate is attractive, but hidden fees can negate savings. Always read the fine print and ask questions if you’re unsure. Have you ever thought about what a small change in your loan terms could mean for your peace of mind? Taking the time to explore refinancing might be the key to keeping your car and reducing stress.Considering Loan Modification

Struggling with car payments can be stressful. Loan modification offers hope. It is a way to adjust your loan terms. This can help you keep your car.

Eligibility Criteria

Not everyone qualifies for loan modification. Lenders have specific requirements. Your financial situation matters. You must show you can’t make current payments. Stable income is important. It proves you can handle new terms. Credit history also plays a role. A history of timely payments can help.

Application Process

Applying for loan modification takes effort. First, contact your lender. Discuss your situation openly. Prepare necessary documents. These include pay stubs and tax returns. A hardship letter is crucial. Explain why you need a modification. Submit the application and wait for a response. The process can take time, so be patient.

Seeking Financial Counseling

Falling behind on car payments can be a stressful experience. As you navigate the financial challenges, seeking professional help might be your best move. Financial counseling offers a path to regain control and avoid repossession.

Finding A Certified Counselor

Locating a certified financial counselor is easier than you might think. Start by checking with reputable organizations like the National Foundation for Credit Counseling (NFCC). Their certified experts can guide you through the process.

Remember to verify the counselor’s credentials. A certified counselor will have the necessary training to provide accurate advice. This step ensures you receive reliable assistance tailored to your situation.

Benefits Of Professional Guidance

Professional guidance can make a world of difference. A counselor can help you develop a realistic budget and payment plan. This proactive approach can prevent future financial pitfalls.

Moreover, a counselor can negotiate with your lender on your behalf. This might lead to more manageable payment terms. It’s a practical strategy that could save your car from repossession.

Have you considered the peace of mind that comes with having a professional on your side? It’s empowering to know you have a plan and support. Professional guidance is a valuable resource during financial hardship.

Alternative Transportation Solutions

Falling behind on car payments can lead to repossession. Typically, missing two or three payments triggers this process. Lenders usually notify borrowers before taking action, providing a chance to resolve the issue.

Finding yourself behind on car payments can be a stressful situation. The looming threat of repossession adds to the anxiety, but there are practical steps you can take to manage your transportation needs. Exploring alternative transportation solutions can offer relief and keep you mobile without breaking the bank.Public Transportation

Public transportation is a reliable and often overlooked option. Buses, subways, and trains provide a cost-effective way to get around. In many cities, monthly passes are available and can save you even more money. Consider the benefits of using public transportation. You can catch up on reading, listen to podcasts, or even get some work done during your commute. Plus, you reduce your carbon footprint. Check local schedules and routes to see how public transport can fit into your daily routine. Many transit apps can help you plan your journey efficiently.Carpooling Options

Carpooling can be a fantastic way to save money and make new connections. Sharing rides with friends, neighbors, or colleagues can significantly reduce your commuting costs. Look for carpooling groups in your area. Social media platforms and community boards often have groups dedicated to organizing carpools. You might be surprised at how many people are looking to share rides. Participating in a carpool not only saves money but also offers a chance to build relationships. You can share stories, discuss common interests, or simply enjoy the company during your ride. Have you considered how these alternative transportation solutions could change your daily life?

Credit: www.creditninja.com

Understanding Your Rights

Understanding your rights is crucial if you’re behind on car payments. Many people face this situation. Knowing your rights can help you manage stress. It can also protect you from unfair practices.

State-specific Laws

Each state has different repossession laws. Some states require a notice before repossession. Others may not. Check your state’s laws to know your rights. This information helps you prepare and plan.

Legal Assistance Resources

Legal help can offer valuable support. Free or low-cost resources are available. Organizations like Legal Aid can assist. They provide advice and guide you. Explore options in your area to get help.

Preventing Future Payment Issues

Falling behind on car payments can disrupt your financial stability. To prevent this, plan for future expenses effectively. Simple strategies can help you avoid the stress of missed payments.

Budgeting Strategies

Create a detailed budget to track your income and expenses. List all monthly bills, including your car payment. This helps you see where your money goes.

Set spending limits on non-essential items. Dining out and entertainment can quickly add up. Being mindful of these expenses helps you save more.

Use budgeting apps or tools. They can automate tracking and provide reminders. This ensures you stay on top of your financial commitments.

Building An Emergency Fund

An emergency fund acts as a safety net. It prevents financial stress during unexpected situations.

Start small by setting aside a fixed amount monthly. Even $20 can accumulate over time. Gradually increase this amount as your financial situation improves.

Keep the fund in a separate account. This minimizes the temptation to dip into it for non-emergencies. Aim for at least three to six months of expenses saved.

Credit: www.greenpath.com

Frequently Asked Questions

How Long Can You Be Late On A Car Payment Before Repo?

Car repossession can start after a payment is 30 days late. Lenders might act sooner based on your agreement. Communicate with your lender to avoid repossession. Always check your contract for specific terms and conditions.

How Long Does It Usually Take For Them To Repossess Your Car?

Car repossession typically occurs after 60 to 90 days of missed payments. Lenders may act sooner based on their policies. It’s crucial to communicate with your lender to avoid repossession. Each lender has different terms, so check your loan agreement for specific details.

How Many Months Behind Can You Be On A Car Payment?

Lenders usually allow one to three months of missed car payments before taking action. After this period, the risk of repossession increases. Always communicate with your lender to explore options if you’re struggling to make payments.

How Behind On Car Payments Before Repossession?

Car repossession usually starts after missing two or three payments. Lenders may initiate repossession sooner based on the agreement. Always check your loan contract for specific terms and communicate with your lender to avoid repossession.

Conclusion

Staying current on car payments is crucial. Missing payments can lead to repossession. Know your lender’s policies. Some act quickly after a missed payment. Communication is key. Talk to your lender if you face difficulties. They might offer solutions. Avoid ignoring calls or letters.

Be proactive. Managing finances wisely helps prevent issues. Set reminders for due dates. Consider automatic payments for convenience. Keep track of your budget. Prioritize essential expenses. Remember, being informed helps you stay on track. Protect your vehicle and credit score.

Make payment arrangements if necessary. Stay vigilant to ensure financial stability.

Ethan Montgomery is the administrator of carweldhub.com and an expert in the automotive industry. With hands-on experience in welding and a deep understanding of automotive parts and accessories, Ethan brings a wealth of practical knowledge to his work. His passion for the automotive field extends to blog writing and editing, where he shares valuable insights and tips with enthusiasts and professionals alike. Whether you’re looking for detailed technical advice or the latest trends in automotive technology, Ethan’s expertise makes him a trusted resource in the automotive community.